Bitcoin ETFs: Should You Own One?

Last week, the SEC approved spot Bitcoin ETFs. Until now, investors wanting exposure to bitcoin could essentially choose between futures or buying directly through an exchange like Coinbase. This barrier to entry and the popularity of Bitcoin has resulted in asset managers launching 11 ETFs designed to track the price of Bitcoin. More are likely to follow. So, investors have a new way to invest in the cryptocurrency that is regulated, transparent, and relatively accessible. Now what?

Does this change anything?

If you were a Bitcoin bull before, this news probably gives you more conviction about its future. And if you were a crypto skeptic, I doubt this news changes much.

The only thing it really changes is the ease of which investors can trade in Bitcoin at current prices. It removes a little friction. Trading Bitcoin is now as cheap and easy as trading shares of your favorite stock or ETF.

Perhaps it expands the potential owners of Bitcoin. Owning part of a Bitcoin isn’t particularly challenging and it can be purchased from a variety of reputable sources including publicly traded (i.e., regulated) companies like Coinbase and PayPal.

Should you buy one? And, from our perspective, should you buy one via a wealth manager (like us!)?

Potential Pros and Cons

Here are my Top 2 arguments for buying a Bitcoin ETF (or Bitcoin more generally).

1) Diversification

Look at the chart below. It illustrates the historical correlation between Bitcoin and stocks, bonds, and real estate. When building a portfolio, including assets with low correlation to one another can potentially reduce volatility and improve long-term compounded returns. Bitcoin has historically checked that box. The average correlation relative to those traditional asset classes, looking at 3-year windows, is basically 0%. If we expect Bitcoin to have good returns going forward, which is obviously up for debate, having no correlation to other assets could be really attractive for investors who hope to reduce the volatility of returns from their portfolio.

Since late 2014, the price of Bitcoin (in USD) has little correlation to other traditional investments like stocks, bonds, and real estate. The chart shows 3-year correlations have consistently been below 25%, and are negative in many cases.

2) FOMO Insurance (aka Regret Avoidance)

FOMO is the Fear Of Missing Out. If you’ve listened to friends or neighbors brag about earning huge returns in something you don’t own, chances are you have experienced FOMO. We face a litany of behavioral biases and emotional struggles when investing. Two of the most common are fear and greed. Perhaps a small investment in Bitcoin or one of the ETFs can remove that fear.

The academic in me, the one who did all the studying and took all the tests, wants to say owning Bitcoin as part of a diversified portfolio is irrational. It’s purely a bet that someone will want to pay me more than what I paid. And yet, I think it could make a lot of sense for people who (a) want to avoid the potential regret of not participating, and (b) are taking a measured risk with capital they can afford to lose without derailing their plans.

Now my Top 2 reasons against buying a Bitcoin ETF:

1) Bitcoin Could Still be a Modern-Day Tulip Mania

Is it rational to think tulip bulbs could rise 12-fold in less than a few months? In the 1600s, it seemed that way to some.

What about the South Sea Company in Britain in the early 1700s? The price quickly rose from £100 to £1,000, just to subsequently (and nearly just as quickly) lose 80% of its value.

Bitcoin has more than its fair share of vocal skeptics. Many are extremely well-respected businesspeople and investors, including perhaps the two most revered investors of our generation, Warren Buffett and his former partner Charlie Munger.

Speculation-driven bubbles have happened many times in the past, only to pop. Human emotions don’t change all that much.

Is Bitcoin just the next example? Time will tell, but anyone considering a Bitcoin investment would be wise to acknowledge the probability of this being the case is something greater than 0%.

2) Own It Directly

Want to own Bitcoin? Then you could always buy actual Bitcoin!

For many investors, owning Bitcoin directly may be preferred. If nothing else, you can potentially avoid the management fees associated with owning the ETFs. The 11 ETFs currently available for purchase charge somewhere between 0.2% and 1.5%. Some of these ETFs are offering lower fees for early investors, too.

I mentioned companies like Coinbase and PayPal earlier. Buying actual Bitcoin is considerably easier and cheaper today compared to 10 years ago.

Lastly, security should be considered. While the ETFs sponsor will choose a custodian to store their bitcoin, those who own directly should think about how and where their bitcoin will be stored.

Why we don’t include bitcoin in our discretionary portfolios

We think it is nearly impossible to forecast, with any degree of certainty, the expected return, volatility, or correlation of Bitcoin to other assets like stocks and bonds. Because of that, we do not include Bitcoin, cryptocurrencies, or other digital assets as part of a strategic asset allocation. We invest in assets (or asset classes) that have existed for decades, having some historical track record that can be analyzed with a reasonable level of reliability. If we were to include Bitcoin (perhaps we will someday) in our portfolios, it would certainly be in what we consider a diversifying sleeve, which is intended to deliver returns that are quite different than those from traditional stocks and bonds. And the ETF is a structure we already understand and like.

Even though we do not include Bitcoin in our investable universe, we strongly believe it’s important for people to be able to include investments like Bitcoin in their portfolio, in a way that feels aligned with long-term goals. To that end, we prefer to carve out a specific piece of the pie within our clients’ Investment Policy Statement to allow for speculative investments. This speculative bucket is behavioral in nature. We don’t expect it to deliver outstanding returns. If it does, we’d prefer to treat these outcomes as happy surprises. We also think people should be prepared to watch these investments disappear entirely. Everyone’s situation is different, but we prefer to stop accumulating speculative assets once they become 10% of someone’s investable assets. You may be comfortable with more. It’s highly personal and everyone’s situation is different. Be aware of the risks and comfortable with the potential losses.

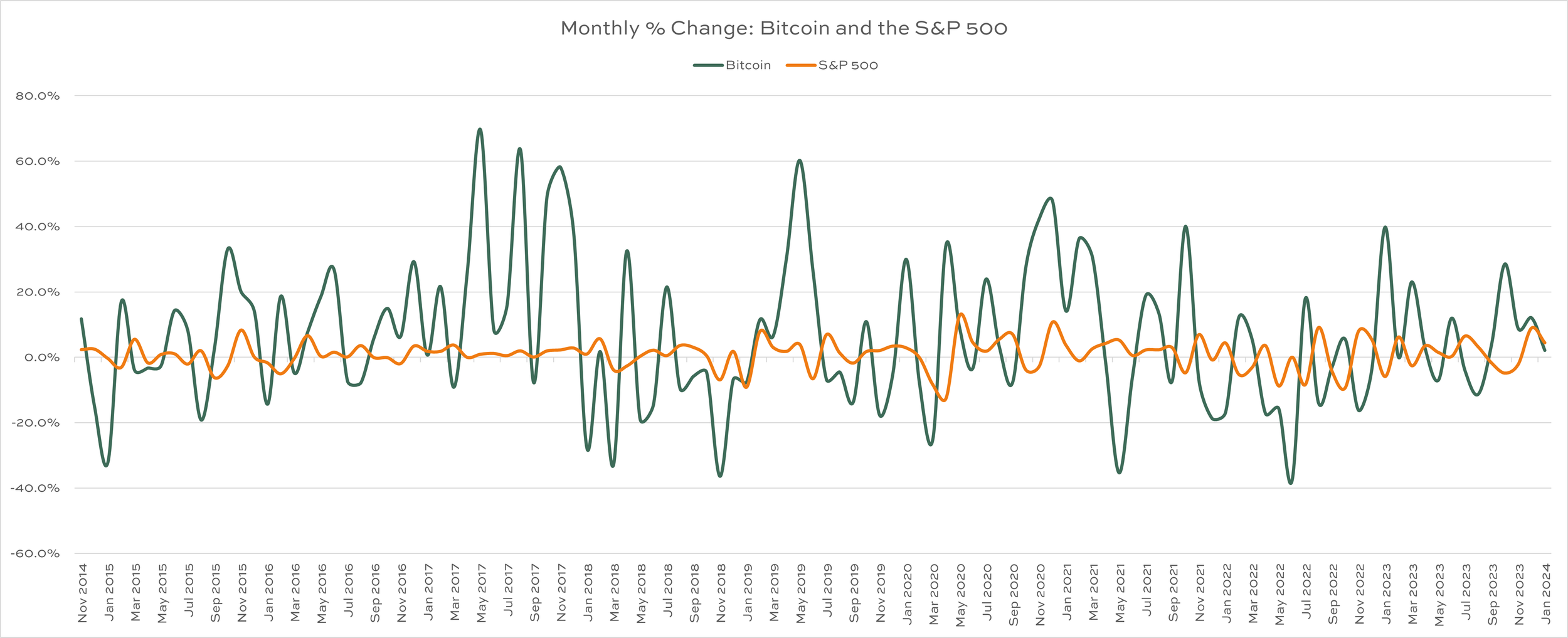

Finally, it’s worth noting this historical volatility of Bitcoin. Look at the two charts below.

The first chart, Bitcoin: % Off High, shows the price drops investors have experienced since 2014. On three separate occasions, the price of Bitcoin fell at least 60% from it’s previous peak! This asset is not for the faint of heart.

The second chart shows monthly returns for Bitcoin (the green line) and the S&P 500 (the orange line). For those who think stocks are volatile, Bitcoin loudly proclaims, “Hold my beer.” Large monthly swings should be expected. Again, if the thought of seeing your investment rise or fall by 20%, 30%, or 40% on a monthly basis, you may wish to avoid Bitcoin and cryptocurrency.

Summary

Regardless, put some thought into this before you buy. Remove emotion. If we know anything about Bitcoin, it’s that the price can move very, very quickly. Put a plan in place before you buy, and revisit it when emotions are running a little hot. It should help make better, or at least more intentional, decisions around your crypto investments.

Divvi Wealth Management (DWM) is a State registered investment adviser. Information presented is for educational purposes only intended for a broad audience. The information does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and are not guaranteed. DWM has reasonable belief that this marketing does not include any false or material misleading statements or omissions of facts regarding services, investment, or client experience. DWM has reasonable belief that the content as a whole will not cause an untrue or misleading implication regarding the adviser’s services, investments, or client experiences. Please refer to the adviser’s ADV Part 2A for material risks disclosures.

Past performance of specific investment advice should not be relied upon without knowledge of certain circumstances of market events, nature and timing of the investments and relevant constraints of the investment. DWM has presented information in a fair and balanced manner.

DWM is not giving tax, legal or accounting advice, consult a professional tax or legal representative if needed.

DWM may discuss and display, charts, graphs and formulas which are not intended to be used by themselves to determine which securities to buy or sell, or when to buy or sell them. Such charts and graphs offer limited information and should not be used on their own to make investment decisions. Consultation with a licensed financial professional is strongly suggested.

The opinions expressed herein are those of the firm and are subject to change without notice. The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions, and may not necessarily come to pass. Any opinions, projections, or forward-looking statements expressed herein are solely those of author, may differ from the views or opinions expressed by other areas of the firm, and are only for general informational purposes as of the date indicated.